Veterans Long-Term Care Benefits Information

The Department of Veterans Affairs (VA) pays for long-term care services for service-related disabilities and for certain other eligible veterans, as well as other health programs such as nursing home care and at-home care for aging veterans with long-term care needs.

The Department of Veterans Affairs (VA) pays for long-term care services for service-related disabilities and for certain other eligible veterans, as well as other health programs such as nursing home care and at-home care for aging veterans with long-term care needs.

The VA also pays for veterans who do not have service-related disabilities, but who are unable to pay for the cost of necessary care. Co-pays may apply depending on the veteran’s income level.

The VA has two more programs to help veterans stay in their homes:

- The Housebound Aid and Attendance Allowance Program. This program provides cash to eligible veterans with disabilities and their surviving spouses to purchase home and community-based long-term care services such as personal care assistance and homemaker services. The cash is a supplement to the eligible veteran’s pension benefits

- A Veteran Directed Home and Community Based Services program (VD-HCBS). This program was developed in 2008 for eligible veterans of any age. The program provides veterans with a flexible budget to purchase services. Counseling and other supports for veterans are provided by the Aging Network in partnership with the Veterans Administration

Many veterans who have savings obtain affordable Long-Care Insurance to safeguard their assets and ease the burden on their families. Vets who have a military pension and TRICARE for their health insurance will still get long-term care insurance (unless they have a full military disability or little or no assets). TRICARE, like any other health insurance or Medicare or Medicare Supplement will only pay for a limited amount of skilled long-term care service and only if a person is improving.

Visit the Department of Veterans Affairs: https://www.va.gov/ to view available programs and services or download a Veterans Benefits fact sheet http://www.benefits.va.gov/BENEFITS/factsheets.asp. You can call the VA at 800-827-1000 to obtain information about services available in your area.

Medicare and Medicaid Coverage Information

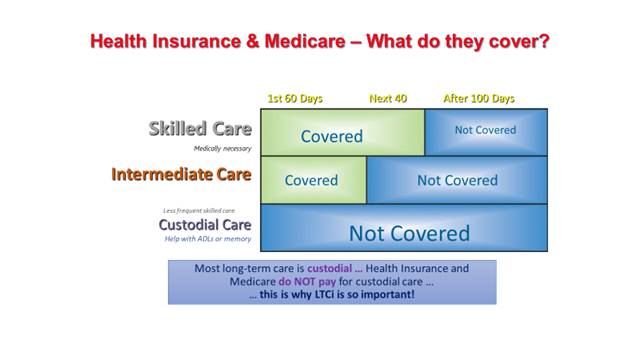

Health insurance, including Medicare and Medicare Supplements (MediGap) will only pay a limited amount of skilled long-term care and only if you are recuperative in nature (meaning you are improving). Most long-term care is custodial in nature (this means help with activities of daily living or supervision due to cognitive issues). Custodial care is NOT covered by any health insurance or any Medicare type of policy. Only affordable long-term care insurance will provide the resources to safeguard your savings and ease the burden extended care places on your loved ones.

Medicaid

Medicaid is a joint federal and state program that helps with medical costs for some people with limited income and resources. Medicaid also offers benefits for long-term care in the event you either have little or no resources or exhaust your savings when you must pay for long-term care costs out-of-pocket. Often, this care is only in a Medicaid nursing home although some states will provide some homecare from Medicaid approved providers.

Many people wish to avoid spending down their hard-earned savings and investments because of a long-term care event. Many states also participate in the federal/state long-term care partnership program which provides additional asset protection. See your state spend down requirements and participation in the partnership program by clicking here: LTC Information By State.

The bottom line: Unless you have affordable long-term care insurance you will have to pay for long-term care out-of-pocket draining your 401(k), IRA 403(b) and other assets and perhaps forcing yourself into a spend-down Medicaid situation.

National Council for Aging has a guide for Veteran’s: Military Veteran Benefit Options