Do I have to report benefits from a Long-Term Care Insurance policy to the IRS?

Generally, no. Tax-qualified Long-Term Care Insurance benefits come to you tax-free. Insurance companies that pay long-term care insurance benefits are required by the Internal Revenue Service (IRS) to provide claimants with a 1099 LTC. This form is used to report the payments made under a long-term care insurance contract. Insurance companies usually issue these 1099 LTC Forms in January for the prior tax year.

The Form 1099-LTC reflects payments made directly to you as well as those payments made to third parties on your behalf. Some people are concerned when they receive these IRS forms in the mail, since the amounts reported to you and the IRS can be very high (as little as $20,000, $100,000, or more). It causes policyholders to wonder about the tax implications of their LTC benefit, however the 1099 forms are required simply to show the IRS you received tax-free benefits from your long-term care insurance policy. It does not necessarily mean that the amount is taxable income to you.

If You Prepare Your Own Tax Forms

Request the Instructions for Form 1099-LTC from the IRS. You can request free tax forms and guides by calling the IRS at 1-800-TAX-Form or 1-800-829-3676.

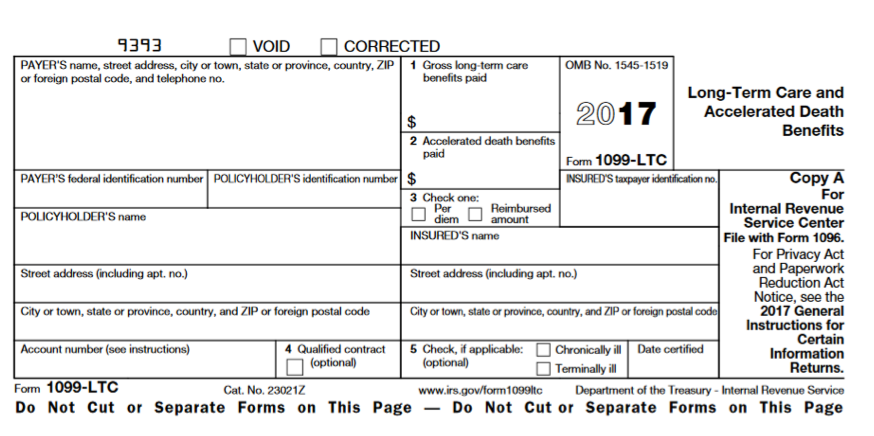

The form looks something like this:

Be sure to speak with your tax advisor. Below is a simple reference of the meaning of numbers reported in each box on the 1099 LTC.

Box 1. Gross benefits paid by the insurance company.

Box 2. Does not apply to long-term care insurance.

Box 3. This indicates benefits paid (as reflected in Box 1) as either on a Per Diem (Indemnity) basis or as a Reimbursement for actual long-term care expenses incurred.

Box 4: This is an optional field that indicates if benefits were paid from a Tax Qualified long-term care insurance contract.

Box 5: The Chronically Ill box will always be checked for LTC. The Terminally Ill box is not applicable to long-term care

PAYER'S NAME: The name of the insurance company and its address.

OMB No.: The tax year for which amounts are reported.

PAYER'S FEDERAL IDENTIFICATION NUMBER: The federal tax identification number for the insurance company that paid the benefit amounts.

POLICYHOLDER'S IDENTIFICATION: The policyholder's identification number, which should be the same as what is in box 10, the insured's Social Security number.

INSURED'S SOCIAL SECURITY: The Social Security number, name and address for the insured who was the recipient of benefits.

Account Number: The actual claim number. This box may also contain the Total Number of Days paid if the policy is an Indemnity (per diem paid) policy.

Date Certified: If the policy uses a Reimbursement formula, this box will show the date certified as Chronically Ill. If the policy uses a Per Diem (indemnity) formula, it will show the claim's original date of loss.

Additional Explanations Regarding Box 3

1. If Box 3 is marked "Reimbursed Amount" and the policy is categorized as a Tax-Qualified Contract, then the amount of money received can generally be excluded from the income being reported. The insurance company can tell you if your policy is considered a Tax-Qualified policy.

A tax-qualified long term care insurance contract qualifies for favorable federal income tax treatment. If the policy only pays benefits that reimburse you for qualified long-term care expenses you will not owe federal income tax on these benefits.

2. If Box 3 is marked "Reimbursed Amount" and you have a Non-Tax Qualified Contract, then some or all of your benefits may be taxable. Again, the insurance company can tell you if your policy is considered a Non-Tax Qualified policy.

A Non-Tax Qualified policy may result in a tax liability. You should consult a tax-advisor. Today, most long-term care policies are tax-qualified.

3. If Box 3 is marked "Per Diem" (which will happen for policies that are considered Indemnity policies) then the amount you may exclude from taxable income being reported is limited.

Because benefits were paid on a per diem (indemnity) basis, without regard to the actual long-term care expenses incurred; the amount of benefits that may be excluded from income is subject to a daily maximum amount.

If this per diem (indemnity) limitation is exceeded, part of the benefits received may be taxable. The amount of the limitation increases every year. If you have that type of policy be sure to consult with your tax advisor.